The world of Accounting revolves around the ‘Debits’ and ‘Credits’. These two have an equal value for a transaction but have an opposite entries. These entries of transactions are to be maintained by each business (Profit or Non-Profit Organization) in the form of accounting books to the interested parties (owners, investors, government departments, etc). In this blog, we will talk in detail about the types of Golden Rules of Accounting.

What are the Golden Rules of Accounting?

Golden Rules of Accounting provides the basis to record all day to day financial business transactions in the Journal Book. Every entry in this book has a Double-Entry System. To understand the Golden rules of accounting, first, we have to know the types of accounts as per the golden rules of accounts because rules are applied to the transaction on the basis of the type of accounts included in the transaction.

Types of Accounts as per Golden Rules of Accounting

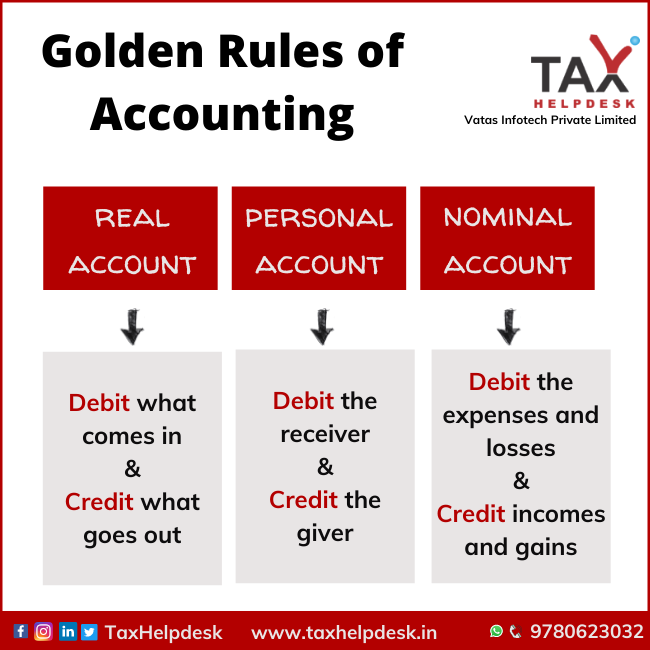

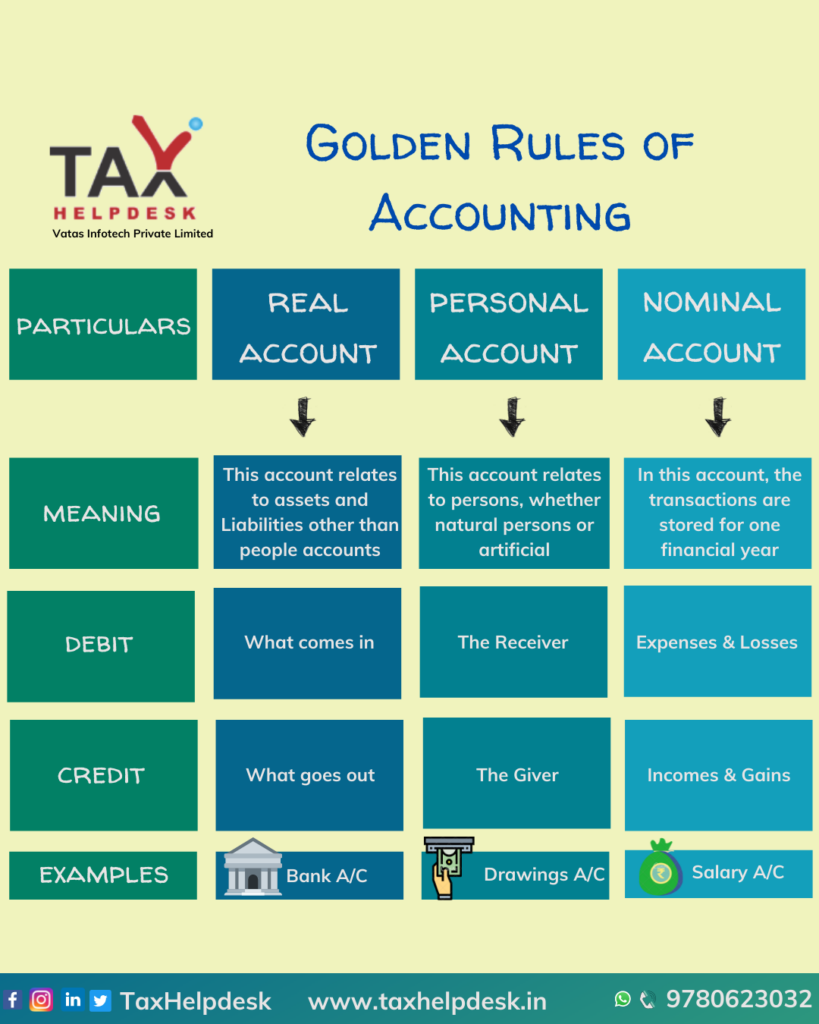

As per the Golden Rules of Accounting, there are three types of accounts namely:

– Real Account

– Personal Account

– Nominal Account

Real Account & Golden Rule 1

A Real Account is a general ledger account that relates to Assets and Liabilities other than people accounts. These accounts do not close at year-end and are carried forward. An example of a Real Account is a Bank Account.

Also Read: 10 Ways to Save Your Taxes!

Golden Rule 1: Debit what comes in, Credit what goes out

In a Real Account, if a business receives something of value (property or goods), it is represented in the books as debited. If something of value goes out from the business it is represented in the books as credited.

Example: Ram deposited cash of Rs. 10,000 in bank on 1st January, 2023

| Date | Particulars | Debit | Credit |

| 01.01.2023 | Bank A/c | Rs. 10,000 | |

| To Cash A/c | Rs. 10,000 |

Personal Account & Golden Rule 2

A Personal Account is also a general ledger account. All accounts related to persons, whether natural persons like individuals or artificial persons like companies, fall under this category. An example of Personal Account is Drawings Account.

Golden Rule 2: Debit the receiver, credit the giver.

In the case of a personal account, when a business receives something from another business or individual, the first business becomes the receiver, and the second business or individual from which it was received becomes the giver.

Example: Lakshman bought gift worth Rs.10,000 from Bharat Shop on 2nd January, 2023

| Date | Particulars | Debit | Credit |

| 02.01.2023 | Purchases A/c | Rs. 10,000 | |

| To Accounts Payable / Bharat Shop | Rs. 10,000 |

Nominal Account & Golden Rule 3

A nominal account is the type of account in which all accounting transactions are stored for one financial year. The balances are transferred to permanent accounts at the end of a financial year. These Nominal accounts are usually related to Revenues, Expenses, Gains and Losses. An example of Nominal Account is Salary Account.

Golden Rule 3: Debit all expenses and losses, credit all incomes and gains.

If a business incurs a loss or expense, then the books’ respective entry is represented as a debit. If the business earns a profit or gains income by way of rendering services, then the entry in the book is represented as credit.

Example: Sita pays business pays rent of Rs. 10,000/- for the premises held by her on 10th day of each month. The entry for month of July will be as follows:

| Date | Particulars | Debit | Credit |

| 01.01.2023 | Bank A/c | Rs. 10,000 | |

| To Cash A/c | Rs. 10,000 |

Conclusion

| Account Type | Particulars involved | Example Account | Example Transaction |

|---|---|---|---|

| Personal Account | Individuals, Entities | Ram’s Account | Received payment from Ram for services rendered |

| Personal Account | Individuals, Entities | Customer Account | Sold goods on credit to a customer |

| Personal Account | Individuals, Entities | Supplier Account | Purchased goods on credit from a supplier |

| Real Account | Assets, Properties | Building Account | Purchased a new building for business operations |

| Real Account | Assets, Properties | Equipment Account | Purchased new machinery for manufacturing |

| Real Account | Assets, Properties | Land Account | Acquired additional land for expansion |

| Nominal Account | Incomes, Expenses | Rent Expense Account | Paid monthly rent for office space |

| Nominal Account | Incomes, Expenses | Sales Revenue Account | Sold products to a customer |

| Nominal Account | Incomes, Expenses | Salary Expense Account | Paid monthly salaries to employees |

These three golden rules of accounting lay the foundation on which the accounting system is standing today. These rules standardise the representation of financial transactions across the industry. Through these rules, it is possible to record each transaction of the business.

Also Read: Best Ways To Save Taxes (Other Than Section 80C)

If you have any suggestions/feedback, then please drop us a message in the chat box. For more updates on Taxation, Financial and Legal matters, join our group on WhatsApp, channel on Telegram or follow us on Facebook, Instagram, Twitter and Linkedin!

Pingback: Fundamentals Accounting Assumptions: An Overview | TaxHelpdesk

Pingback: Types of Golden Rules of Accounting | TaxHelpde...