National Pension Scheme or NPS was introduced in January, 2004 and is regulated by Pension Fund Regulatory and Development Authority(PFRDA). It was initially applicable to government employees but in the year 2009, it was opened to all the classes of the employees apart from the armed forces. This scheme is mandatory for the government employees and other employees have a choice to invest in NPS.

Under this scheme, the individuals are encouraged to invest in a pension account at regular intervals during the course of their employment. On retirement, a certain percentage of amount can be withdrawn and the remaining amount can be used for purchasing an annuity.

Who can invest in National Pension Scheme?

Any individual – resident or non resident aged between 18 to 60 years can invest in the National Pension Scheme. It is a good option to invest in for all those individuals who has got low risk facing capacity and wants to plan their retirement on a planned basis. The income invested today in this scheme can be utilized at the time of retirement.

National Pension Scheme Income Tax Benefits

As per the provisions of Income Tax Act, an individual can claim deductions under the following sections by investing in National Pension Scheme:

– Section 80CCD(1)

– Section 80CCD(2)

– Section 80CCD(1B)

National Pension Scheme under Old & New Tax Regime

Before expaining in detail the provisions related to Income Tax benefits on investments in NPS, it must be noted that deduction under Section 80CCD(1) is only available under the Old Tax Regime.

Also Read: Comparison of Exemptions & Deductions under the Old & New Tax Regime

But, for those employees, whose employer is contributing to its National Pension Scheme or NPS account, income tax deduction under Section 80 CCD (2) is available even when they have chosen New Tax Regime.

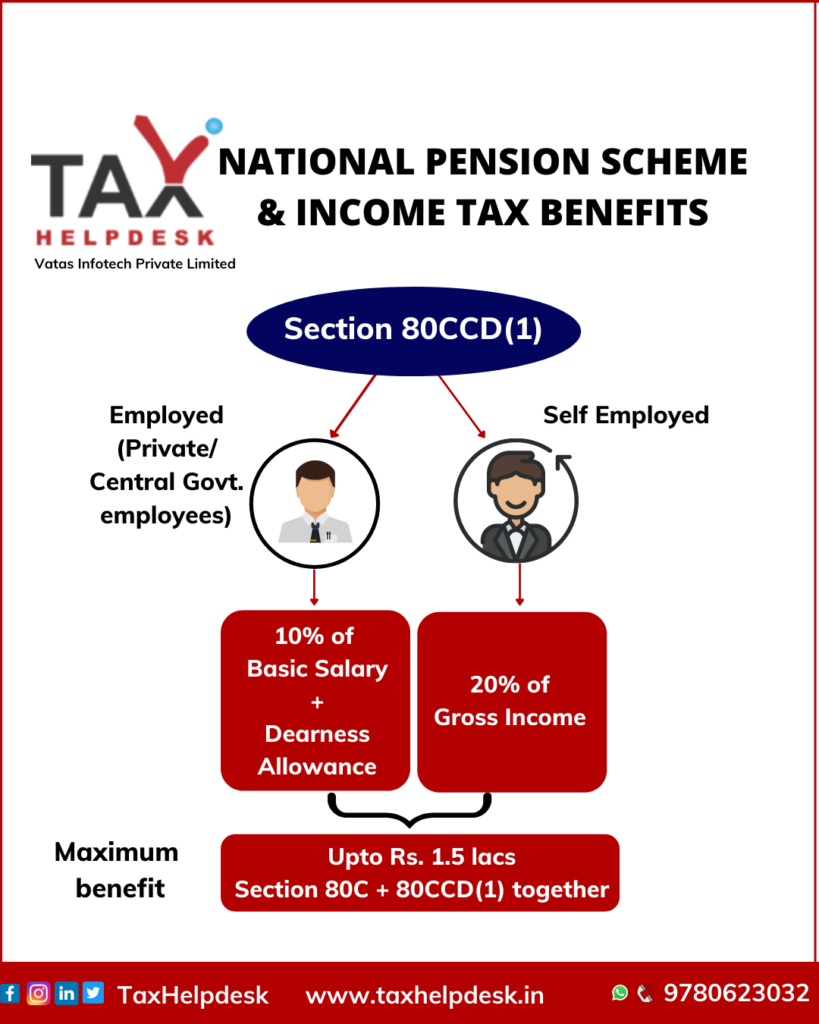

Section 80CCD(1)

The deduction on NPS under Section 80CCD(1) can be claimed by Salaried Individual (except Central Government employees)

Under Section 80CCD(1), the individuals can be distinguished on the basis of salaried and self employed.

– Salaried individuals can contribute to NPS of up to 10% of their basic salary.

– Self employed individuals can contribute to NPS of up to 20% of their basic salary.

Also Read: Do I need to file Income Tax Return

Note

The maximum deduction that can be claimed is ₹1.5 lacs Section 80C + 80CCD(1) put together.

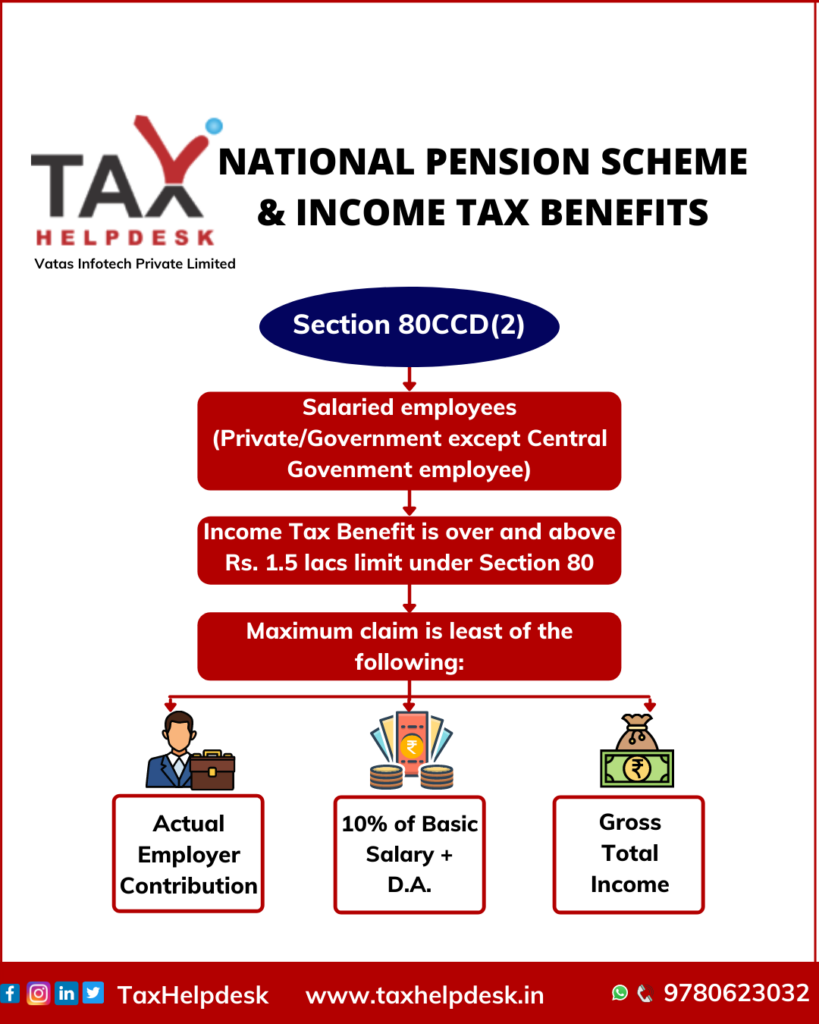

Section 80CCD(2)

This tax deduction on NPS Investment under Section 80CCD(2) can be claimed by Individuals other than Central Government employees

– Under the NPS, the employer can also contribute towards this scheme.

– This contribution made by employer can be claimed as tax deduction.

– The maximum amount which can be availed as deduction is the least of following

– Actual contribution by the employer

– 10% of basic salary

– Gross total income

Note:

– This contribution amount to be claimed as deduction is exclusive of the amount of deduction under Section 80C of the Act.

– Self employed individuals cannot claim this deduction.

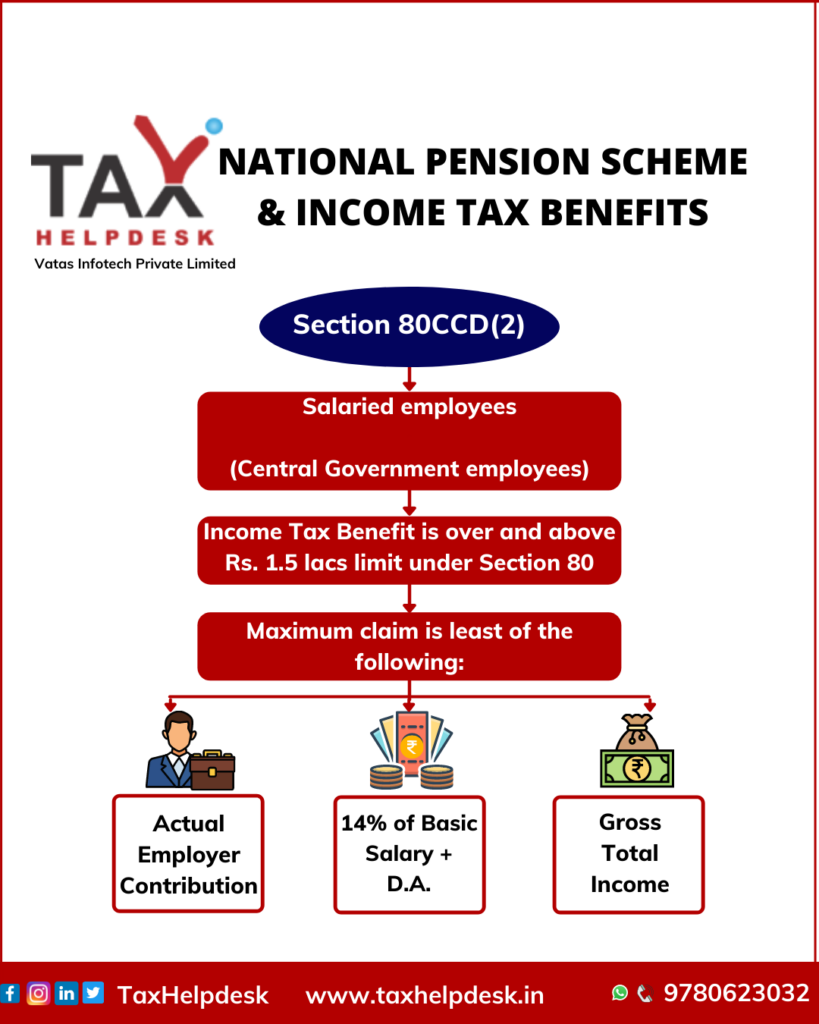

Section 80CCD(2)

Tax deduction under Section 80CCD(2) on NPS Investment can be claimed by Central Government employees

Under the NPS, the employer can also contribute towards this scheme. This contribution made by employer can be claimed as tax deduction.

The maximum amount which can be availed as deduction is the least of the following

– Actual contribution by the employer

– 14% of basic salary (earlier it was 10%)

– Gross total income

– This contribution amount to be claimed as deduction is exclusive of the amount of deduction under Section 80C of the Act.

Important Note:

If you are selecting New Tax Regime in your Income Tax Return, then now there is a threshold limit under Section 80CCD(2), w.e.f., AY 2021-22. Your employer can contribute to your NPS account as mentioned in the above points. However, if your employer’s contributions under Section 80CCD(2) are more than ₹7,50,000 a year (along with EPF and Superannuation), then such exceeding contributions are taxable income in the hands of the employee. The interest earned on over and above ₹7.5 lakh balance is also taxable.

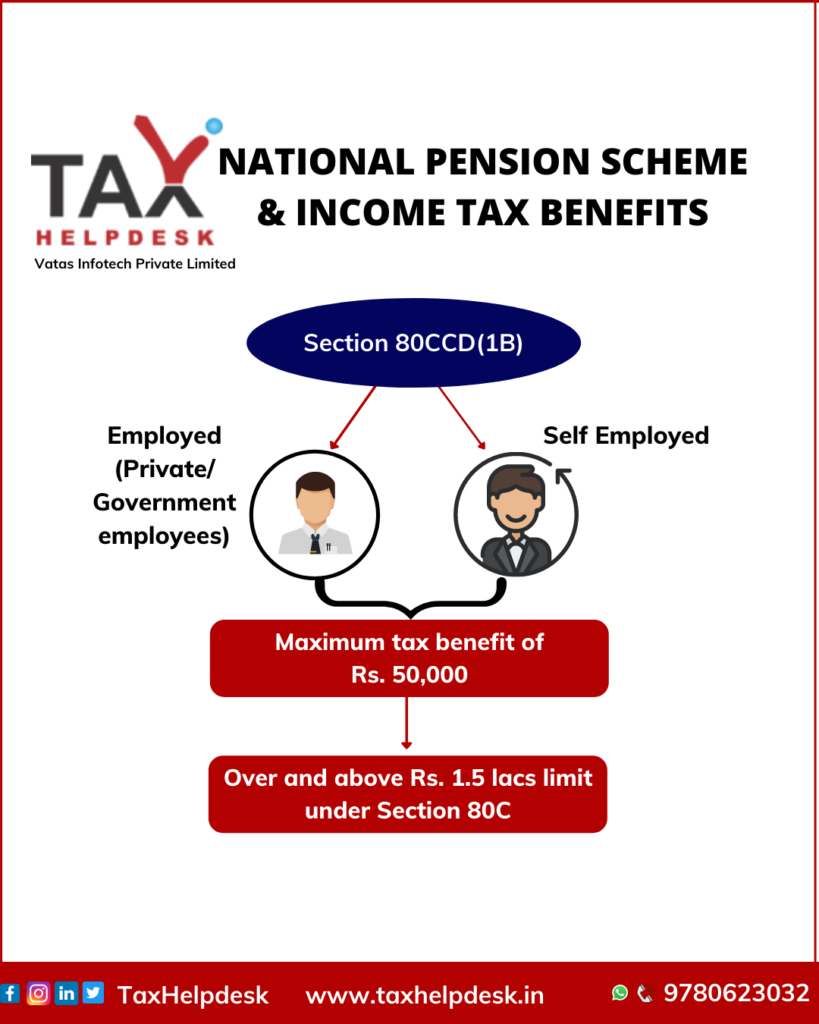

Section 80CCD(1B): NPS additional tax deduction

Section 80CCD(1B) provides additional Income Tax deduction on NPS investments to all the employees.

Under Section 80CCD(1B), an additional tax deduction of ₹50,000/- can be claimed by the salaried or self employed individuals.

NOTE:

Total deductions under Section 80C, Section 80CCC and Section 80CCD(1) together cannot exceed the threshold limit of ₹1.50 lacs for any financial year.

On the other hand, the additional tax benefit of ₹50,000/- under Section 80CCD(1B) is over and above the above limit of ₹1.5 lacs.

How to invest in National Pension Scheme?

The NPS offers government bonds, corporate and equity related options as the main fund driving instruments and is structured in two mechanisms or tiers, which are referred to as tier 1 and tier 2.

| Aspect | Tier-I Account | Tier-II Account |

|---|---|---|

| Purpose | Retirement corpus and pension after retirement | Savings and investment |

| Mandatory/Optional | Mandatory | Optional |

| Tax Benefits | Eligible for tax deductions under Section 80CCD(1) and additional deduction under Section 80CCD(1B) | No additional tax benefits |

| Contribution Limits | Subject to the minimum and maximum limits set by the NPS | No specific limits |

| Withdrawal Restrictions | Partial withdrawals allowed under specific circumstances and subject to conditions | No restrictions, easy withdrawals possible |

| Lock-in Period | Lock-in until the age of 60, with limited exceptions for premature withdrawal | No lock-in period |

Therefore, in order to claim the deductions of NPS, the individual will have to open Tier-I account. All the above mentioned deductions are exempted from tax only on NPS Tier-I account. Under the NPS Tier-II account, there is no deduction available apart from the contributions made by the government employees under Section 80C of ₹1.50 lacs.

If you have any suggestions/feedback, then please leave the comment below. For more updates on Taxation, Financial and Legal matters, join our group on WhatsApp or follow us on Facebook, Instagram and Linkedin!

Pingback: 10 Ways to Save Your Taxes! | TaxHelpdesk

There are some interesting points in that clause but I dont know if I see all of them eye to centre . There is some validness but I will take hold legal opinion until I look into it further. Good clause, thanks and we want more! Added to FeedBurner besides.

Pingback: Know Changes in EPF Contribution Taxability | TaxHelpdesk