Employees Provident Fund or EPF is savings cum retirement scheme for the salaried individuals. Under this scheme, contribution is made both by the employer and the employee. The amount contributed in EPF scheme is 12% of the salary (basic + dearness allowance). The amount invested over the years, along with specified interest, is paid out to an employee on his/her retirement.

Note:

Only 3.67% of the employer’s contribution goes towards Employees’ Provident Fund (EPF) account. And, rest of the 8.33% gets deposited in the Employees’ Pension Scheme.

Contribution to EPF

As stated above, the contribution to EPF is two-fold:

– Employer contribution and

– Employee contribution.

The employee contribution is eligible for deduction under Section 80C of the Income Tax Act, 1961. Meaning thereby, the contributions made by the employer on behalf of the employee is

– free from tax,

– the interest earned on the said contribution is tax-free, and

– the withdrawals from the fund are also tax-free subject to certain conditions.

Having said that, the accumulated balance due and becoming payable to an employee participating in a recognized EPF shall be tax-free in the following cases –

(i) If the employee has rendered continuous service with his employer for a period of 5 years or more, or

(ii) If, though he has not rendered such continuous service of 5 years, the service has been terminated

(a) by reason of such an employee’s ill health or

(b) by the contraction or discontinuance of the employer’s business or

(c) or other cause beyond the control of the employee, or

(iii) If, on the cessation of his employment, the employee obtains employment with any other employer. Even more, to the extent the accumulated balance due and becoming payable to him is transferred to his individual account in any recognized fund maintained by such other employer.

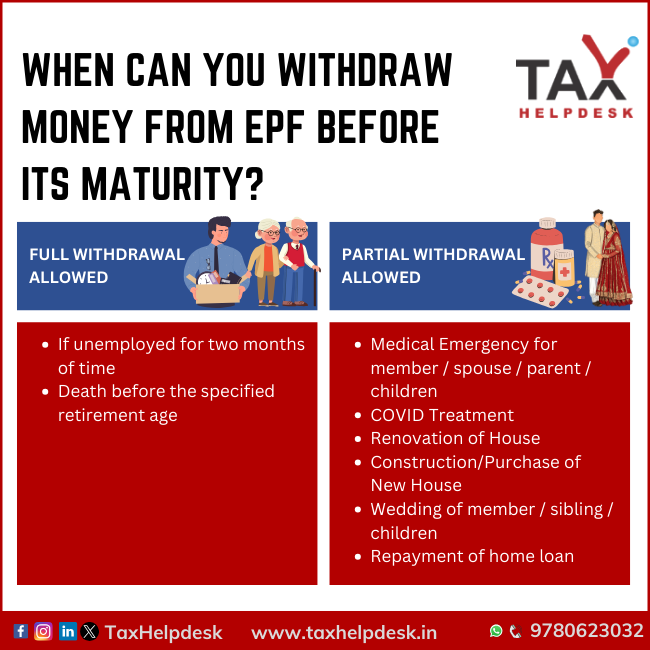

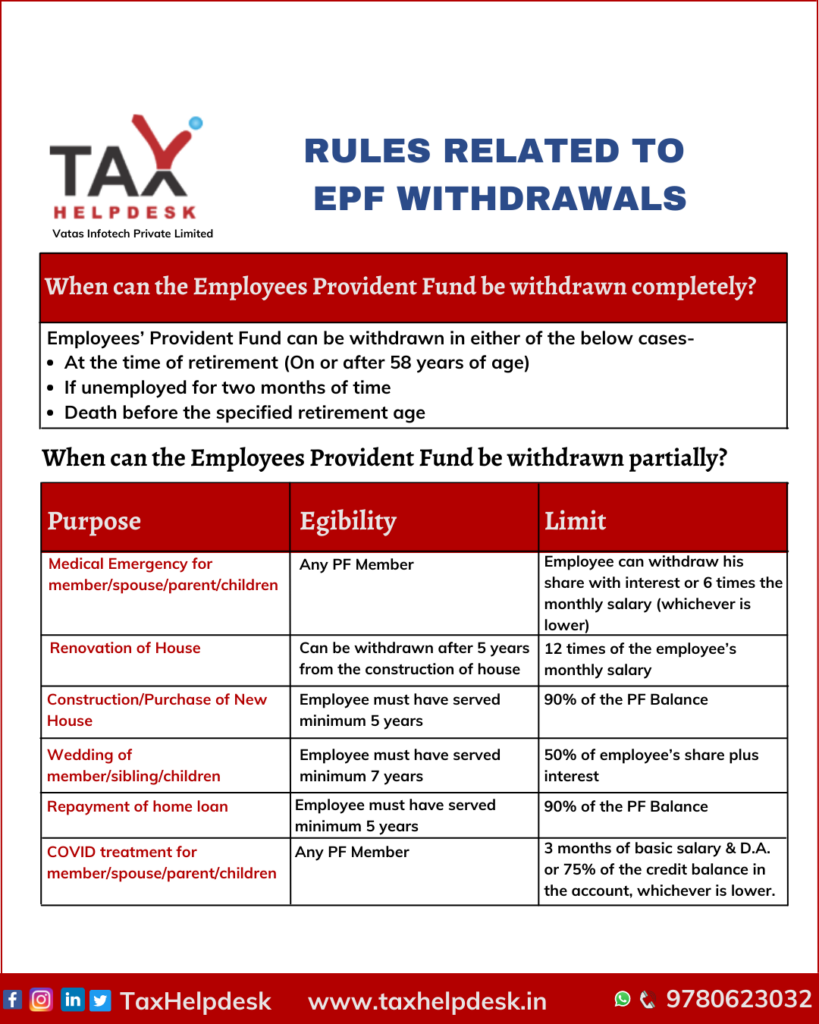

When can the amount in EPF be withdrawn?

Employees’ Provident Fund can be withdrawn partially or completely.

EPF withdrawal online can be done completely in either of the below cases:

– At the time of retirement (On or after 58 years of age)

– If unemployed for two months of time

– Death before the specified retirement age

Rules related to EPF Withdrawals

Cases where EPF can be withdrawn partially

For Medical Purposes:

An employee is allowed to withdraw employee’s share with interest or six times the monthly salary (whichever is lower) from the provident fund for the purpose of medical treatment. This withdrawal is applicable for medical treatments of self, spouse, children, and parents and there is no lock-in period or minimum service period for this type of withdrawal.

Also Read: New Rules Related To Employee Provident Fund Scheme

For Covid Treatment

The EPF member can withdraw EPF amount for treatment of Covid of self/spouse/childern/parents. The amount that can be withdrawn is three months of basic salary and dearness allowance or 75% of the credit balance in the account, whichever is lower.

For Repaying Home Loan:

In case of outstanding home loan, the PF member is allowed to withdraw up to 90% of the PF Fund if the house is registered in his or her name or is held jointly. In order to withdraw the amount for this purpose, at least 3 years of complete service is required

For Wedding:

To claim PF withdrawal for wedding purpose, at least 7 years of service must be completed. Further, the amount that can be withdrawn is 50% of the employee’s contribution with interest and it can be withdrawn for his own, siblings or child’s marriage

Also Read: Everything You Need To Know About Tax Saving Fixed Deposits

Some more rules related to EPF Withdrawal

For Renovating and Reconstructing a House:

The employee can withdraw 12 times his monthly salary from his EPF account for the purpose of renovation and reconstruction. In order to withdraw this amount, following conditions must be met:

– The house should be held in his/her name or held jointly with the spouse.

– He/she must complete at least 5 years of total service

For Purchasing or constructing a New House:

A PF member can withdraw a partial amount from his employee provident fund for the purpose of purchasing a plot and/or constructing if

– The property is registered in his or her name or held jointly with the spouse

– He/she has completed a minimum of 5 years of total service

The amount that can be withdrawn for this is 24 times of the monthly salary for purchasing a plot/36 times of the monthly salary. In addition, for purchasing or constructing a house or the cost of the property or the total of employee’s and his employer’s share. Even more, along with the interest amount (whichever is less) can be withdrawn and can be availed only once in the entire service tenure

Retirement:

A person can withdraw his or her entire provident fund corpus after completing 58 years of age. Furthermore, he is allowed to withdraw up to 90% of the provident fund balance

Also Read: Major Exemptions & Deductions Availed By Taxpayers In India

Unemployment:

A person can withdraw 75% of his or her provident fund if he/she is unemployed for more than a month. In addition to this, in case of unemployment of more than 2 months, remaining 25% of the corpus can be withdrawn

Premature withdrawal of EPF

| Purpose | Eligibility | Limit |

|---|---|---|

| Medical Emergency for member / spouse / parent / children | Any EPF Member | Lesser one of employee’s share plus interest or 6 times of the monthly salary |

| For treatment of Coronavirus of member / spouse / parent / children | Any EPF member | Lesser of up to three months’ worth of basic pay and dearness allowances, or up to 75 percent of the balance in EPF account |

| Construction/Purchase of New House | Employee must have served min 5 years | 90% of the PF Balance |

| Renovation of House | Can be withdrawn after 5 years from the construction of house | 12 times of the employee’s monthly salary |

| Repayment of Home Loan | Employee must have served for min 3 years | 90% of the PF Balance |

| Wedding of member/sibling/children | Employee must have served for min 7 years | 50% of employee’s share plus interest |

Some important points related to EPF Withdrawal Rules

Employees’ Provident Fund is a savings investment scheme created for the purpose of retirement. Furthermore, withdrawal should be prevented until and unless it is an emergency. However, in case a member wants to withdraw funds from his EPF account, he should keep the following EPF withdrawal rules in mind-

– Provident Fund that is withdrawn within 5 years of account opening is taxable

– It’s not necessary to withdraw provident fund when you change your employer as PF can easily be transferred to a new account through the online process

– As per the rules, one cannot withdraw Provident Fund balance of a job where he us currently employed

– Loan (Partial withdrawal) can be availed on Employee Provident Fund

If you have any suggestions/feedback, then please drop us a message in the chat box. For more updates on Taxation, Financial and Legal matters, join our group on WhatsApp, channel on Telegram or follow us on Facebook, Instagram, Twitter and Linkedin!

The views of the author are personal. TaxHelpdesk does not owe any responsibility towards anyone with regard to this blog!

Pingback: New Rules Related to Employee Provident Fund Scheme | TaxHelpdesk

Pingback: Tax Benefits on Health Insurance and Medical Expenditures | TaxHelpdesk