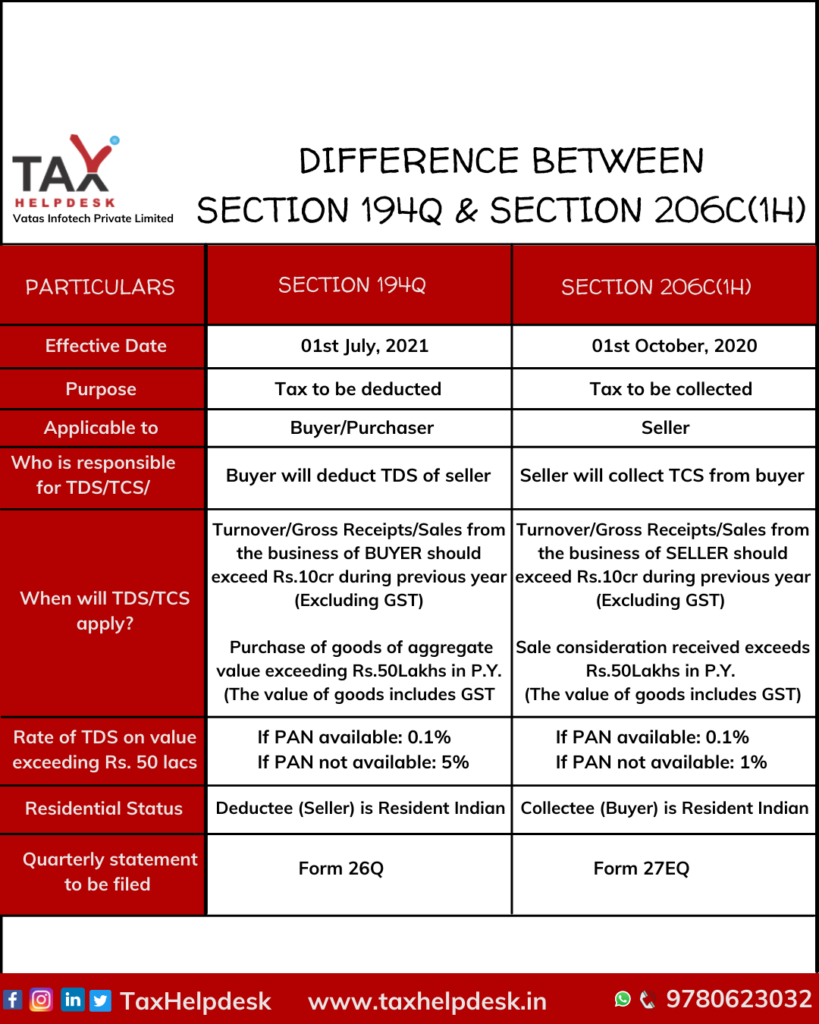

Through the Union Budget, 2021, a new section namely Section 194Q was inserted in the Income Tax Act and this section is similar to the provisions of Section 206C(1H) of the Act. This is so because both of these sections deals with same transaction of sales/purchases above Rs. 50 lacs from party whose turnover whose turnover is previous year exceeds Rs. 10 crore. Further, Section 194Q talks about deducting TDS and Section 206(1H) talks about collecting tax.

Now comes the confusion, whether TDS under Section 194Q is to be deducted by the buyer or TCS under Section 206C(1H) is to be collected on sale of goods? Read this blog ahead to eliminate all your confusions!

Section 194Q

Section 194Q provisions states that, ‘Buyer’ who is responsible for paying any sum to any resident (‘Seller’) for purchase of any goods of the value or aggregate of such value exceeding Rs. 50 lacs during the year, shall deduct TDS @ 0.10%, on amount exceeding Rs. 50 lacs.

Section 206C(1H)

Section 206C(1H) – TCS provision are made applicable on `Seller of Goods’ who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding Rs. 50 lacs during a financial year.

This Section further states that buyers means any person who purchases any goods, subjected to certain exclusions.

Also Read: TDS On Cash Withdrawal From Bank In A Financial Year

Who is a buyer?

Under Section 194Q, ‘Buyer’ means a person whose total sales, gross receipts or turnover from the business carried on by him exceed Rs.10 crore during the financial year immediately preceding the financial year in which the purchase of goods is carried out.

Who is a seller?

The word ‘Seller’ is not been under Section 194Q but as per Section 206C(1H) “Seller” means a person whose total sales, gross receipts or turnover from the business carried on by him exceed Rs.10 crore during the financial year immediately preceding the financial year in which the sale of goods is carried out.

In simple words, Buyer or Seller means a person whose total sales / gross receipts / turnover from business exceeds Rs. 10 crore in the previous year.

Difference between Section 194Q & Section 206C(1H)?

Why was there need to insert Section 194Q when Section 206C(1H) was already there?

The definition of ‘Seller’ under Section 206C(1H) has a very limited scope. There were cases where consideration received during the year exceeded Rs. 50 Lacs but TCS provision was not applicable because Sales / turnover / receipts from business was less than Rs. 10 crore in last year.

Also Read: Pay Double TDS On Non-Filing Of ITR

Government had to visualize this situation and brought those type of transactions within the ambit of tax collection / deduction and thereby, introduced section 194Q by Finance Act, 2021.

The provisions of Section 194Q are similar to the provisions of Section 206C(1H) however, both of these sections are mutually exclusive. This means that if Section 194Q is applicable, then Section 206C(1H) will not be applicable and vice versa.

As per section 206C(1H), TCS will not be applicable if buyer is liable to deduct TDS under any other provisions of the Act. On the contrary, section 194Q does not have any such exception for the transactions on which tax is collectible under section 206C(1H).

Also Read: Restriction On Cash Transactions Under The Income Tax Act

If both Section 194Q and Section 206C(1H) are applicable, then Section 194Q shall supersede Section 206C(1H)

Section 194Q will not apply if:-

– Tax is deductible under any of the provisions of this Act,

– Tax is collectible under the provisions of section 206C other than a transaction to which section 206C(1H) applies.

Section 206C(1H) will not apply if :-

– Where consideration is received on account of export of goods out of India,

– Goods covered under Section 206C(1) such as tendu leaves, timber, scrap, alcoholic liquor for human consumption, minerals, etc

– Goods being Motor vehicle as specified under Section 206C(1F)

– Goods being money received by authorized dealer for remittance as specified under Section 206C(1G)

– If the buyer is liable to deduct TDS under any other provision of this Act on the goods purchased by him from the seller and has deducted such amount

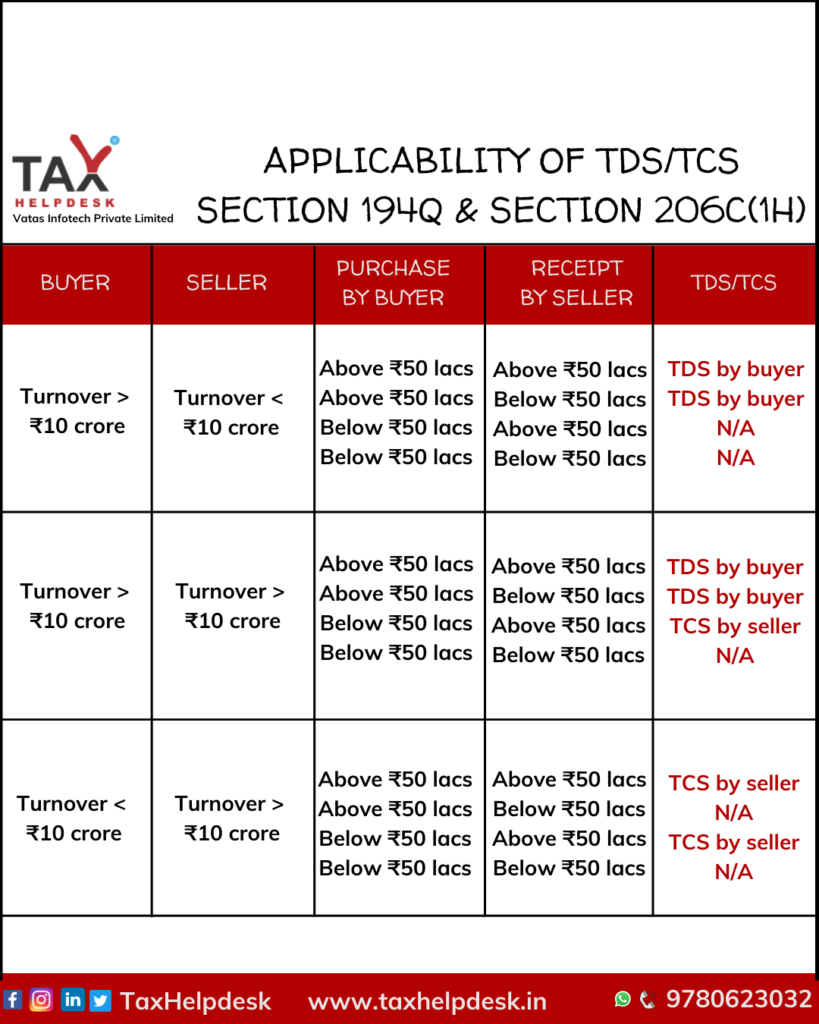

Situations for the applicability of Section 194Q & Section 206C(1H)

Illustration

| Seller turnover | Buyer turnover | Purchases made | Receipt for sales | Responsible person | Amount on which tax will be calculated | Seller PAN | Buyer PAN | TDS under Section 194Q | TCS under Section 206C(1H) | Section Applicable | Reason |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ₹7 crores | ₹11 crores | ₹55 lacs | ₹60 lacs | Buyer | ₹5 lacs | Available | Not Available | 0.10% | Not Applicable | Section 194Q | Seller turnover is less than ₹10 crores |

| ₹8 crores | ₹14 crores | ₹60 lacs | ₹60 lacs | Buyer | ₹10 lacs | Not Available | Not Available | 5% | Not Applicable | Section 194Q | Seller turnover is less than ₹10 crores |

| ₹11 crores | ₹13 crores | ₹54 lacs | ₹52 lacs | Buyer | ₹4 lacs | Available | Available | 0.10% | Not Applicable | Section 194Q | Exclusion provided under Section 206C(1H) |

| ₹11 crores | ₹13 crores | ₹45 lacs | ₹52 lacs | Seller | ₹2 lacs | Not Available | Available | Not Applicable | 1% | Section 206C(1H) | Purchases are less than ₹50 lacs |

| ₹11 crores | ₹13 crores | ₹48 lacs | ₹49 lacs | Not Applicable | Not Applicable | Not Applicable | Not Applicable | Not Applicable | Not Applicable | Not Applicable | Purchase and sales are less than ₹50 lacs |

| ₹16 crores | ₹9 crores | ₹62 lacs | ₹60 lacs | Seller | ₹10 lacs | Not Available | Available | Not Applicable | 0.10% | Section 206C(1H) | Buyer turnover is less than ₹10 crores |

| ₹18 crores | ₹9 crores | ₹53 lacs | ₹55 lacs | Seller | ₹5 lacs | Not Available | Not Available | Not Applicable | 1% | Section 206C(1H) | Buyer turnover is less than ₹10 crores |

If you have any questions, then simply drop a message in the chatbox or leave a comment in the comment box. You can also drop us a message on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Pingback: TDS on Purchase of Goods under Section 194Q | TaxHelpdesk

Pingback: Pay Double TDS on Non-Filing of ITR | TaxHelpdesk