Education is a basic necessity for each individual in any country. Even the Constitution of India says that the right to education is a fundamental right but of the children in the age group of 6 to 14 years. The children of this age group are entitled to free education in government schools. Now this leads us to the question, what children who want to go for higher education and have not enough funds to take the admission? The answer to this question lies in the provisions of Section 80E of the Income Tax Act.

What is Section 80E?

As per the provisions of Section 80E of the Income Tax Act, the interest paid on education loan paid on higher education (including vocational studies) can be claimed as a deduction from the taxable income.

Also Read: 10 Ways To Save Your Taxes!

Note:

The loan for higher education is not based on place and can be taken for education at colleges/university in India or outside India.

Who can avail the deduction of Section 80E?

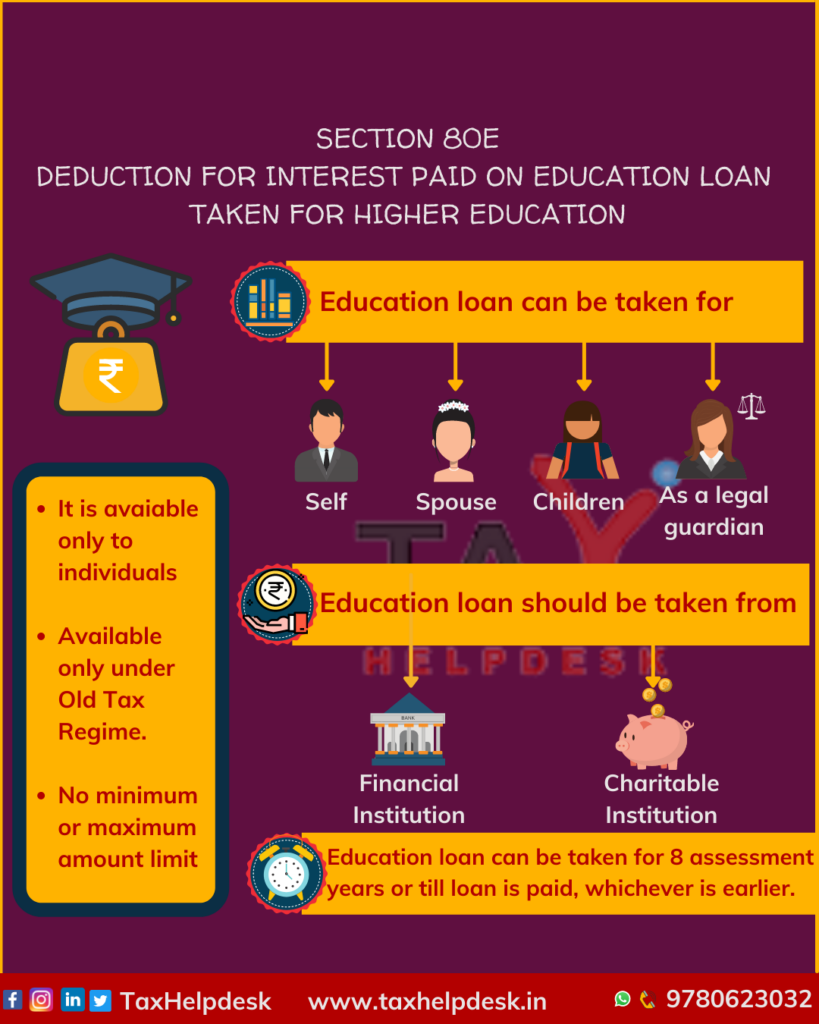

In order to claim the deduction of Section 80E, the person must be an individual who has opted for old tax regime. In other words, this deduction cannot be claimed by HUFs, companies, firms or any other legal personality and individuals opting for new tax regime.

For whom education loan can be taken?

The deduction under Section 80E on repayment of education loan can be claimed by the individual for

– Self,

– Spouse,

– Children, and

– A person for whom he / she is a legal guardian.

Also Read: How to claim rebate of Rs. 12,500

The individual who is repaying the loan for the above mentioned people can take benefit of 80E deduction.

Note:

If the parents of individual are sharing the EMI payments, then the extent to which parents are paying interest part of EMI can be claimed by them and rest by the individual, subject to fulfilment of other conditions.

How to avail the education loan to claim deduction of Section 80E?

In order to claim the deduction of Section 80E, the education loan must be taken from notified:

– Financial institution, or

– Charitable institution: Therefore, if you take loan from your relative or employer for higher education, then you will not be able to claim deduction under Section 80E.

What all documents are to be submitted for claiming deduction of Section 80E?

The deduction of Section 80E can be claimed at the time of filing of Income Tax Returns and it does not require submitting of any documents. However for the purposes of record, following documents must be kept safely, which can be used be at the time of any future scrutiny:

– Documents sanctioning the education loan

– The repayment statements from the financial institution or charitable institution. Such statements should have a clear bifurcation of principal and interest amount repaid.

Also Read: Section 80D: Deductions On Medical Expenditure & Health Insurance

In case of salaried person, the repayment statements from the financial institution or charitable institution must be submitted to the employer, so that the amounts can be shown in Form 16.

For How Much Can You Claim The Deduction Of Section 80E?

The deduction under Section 80E can be claimed for a period of 8 Assessment Years or till the loan amount is paid, whichever is earlier.

For instance,

Karishma has taken an education loan in AY 2022-23 and start paying interest in the same year.

In this case, she can claim a deduction under Section 80E for AY 2022-23 to AY 2029-30 (i.e. 8 assessment years).

Now consider a different situation in which Karishma has repaid the complete loan in 5 years only.

In this case, she can claim a deduction under Section 80E for AY 2022-23 to AY 2027-28 (i.e. till completion of loan).

Maximum/Minimum amount of deduction that can be availed under Section 80E?

There is no maximum or minimum amount of deduction that be claimed under section 80E. The amount of deduction on interest payment deduction is not impacted by the rate of interest charged by the financial or the charitable institution, amount of loan or any other factor. Further, Section 80E is also not impacted by the maximum deduction of Rs. 1.5 lacs available under Section 80C.

| Particulars | Amount |

|---|---|

| Gross Income | Rs 10,00,000 |

| Less: Interest repaid on Education Loan (Deduction under Section 80E) | Rs 5,00,000 |

| Net Taxable Income | Rs 5,00,000 |

The interest repaid on education loan (Rs. 5,00,000) on education loan is subtracted from the gross total income (Rs. 10,00,000). As a result of which the taxable income is reduced to Rs 5,00,000.

If you still have doubts regarding Section 80E, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!

Pingback: Deductions on Interest on Deposits in Savings Account: Section 80TTA | TaxHelpdesk

Pingback: Deduction on Electrical Vehicle for Interest Paid on Loan | TaxHelpdesk

Pingback: Section 80G: Deductions on Donations | TaxHelpdesk

Pingback: 10 Ways to Save Your Taxes! | TaxHelpdesk

Pingback: Know About Systematic Investment Plan (SIP) | TaxHelpdesk