India likely to have double digit growth in FY21-22

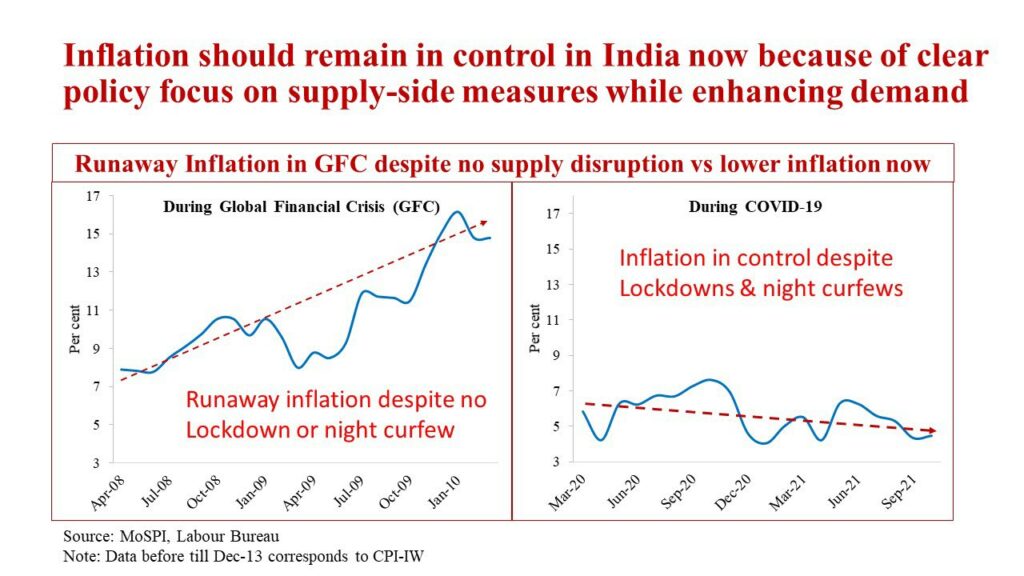

1. India’s policy focused on both Supply & demand to ensure inflation under control. In contrast, post GFC, runaway inflation manifested because of the policy focused only on demand.

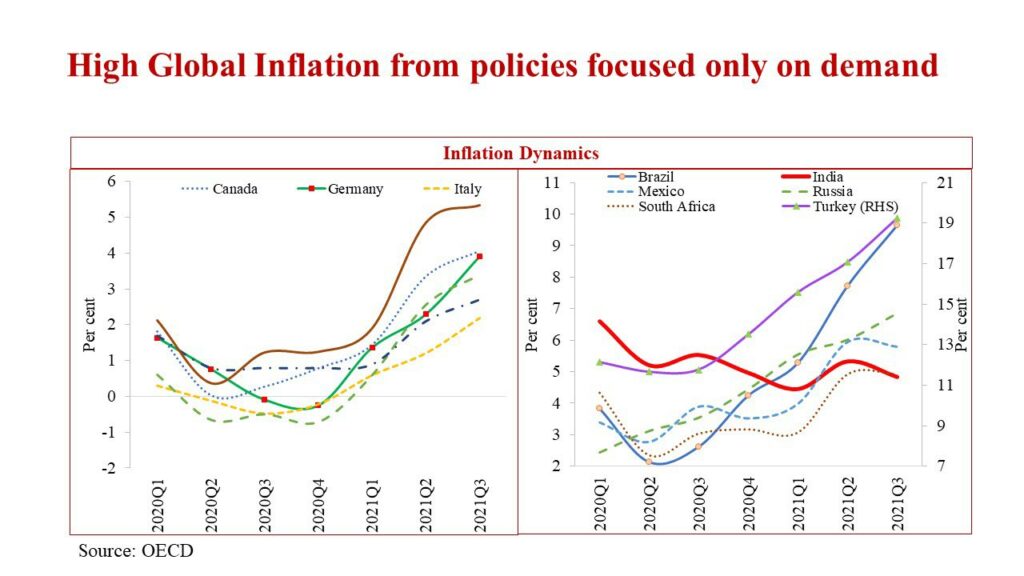

2. Global inflation stems similarly from exclusive focus on demand in contrast to India, where the focus has been on both demand and supply

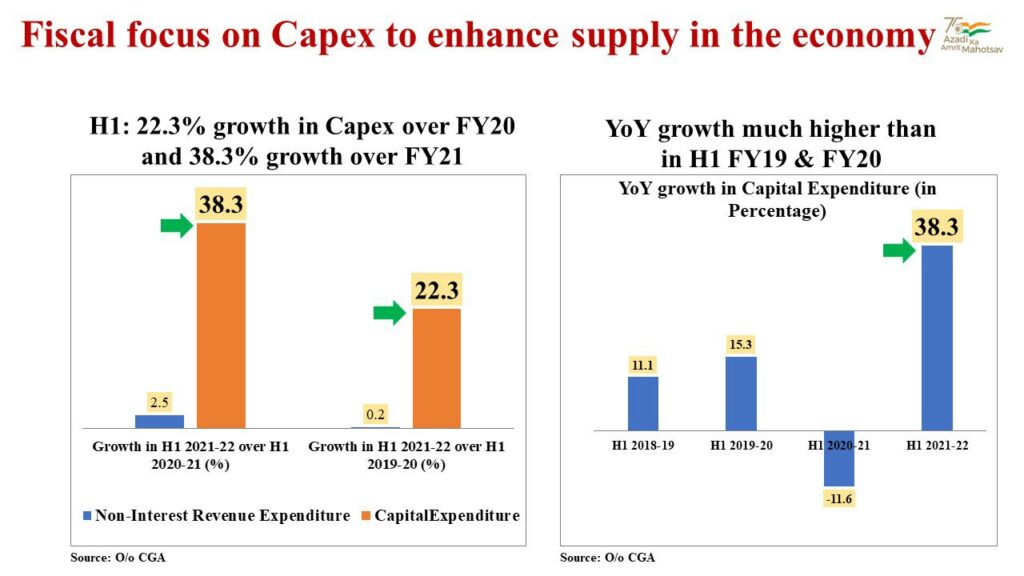

3. Fiscal focus on capital expenditures has ensured that capital expenditures in H1-FY22 have grown at 38.3% compared to H1-FY21 and 22.3% compared to H1-FY20.

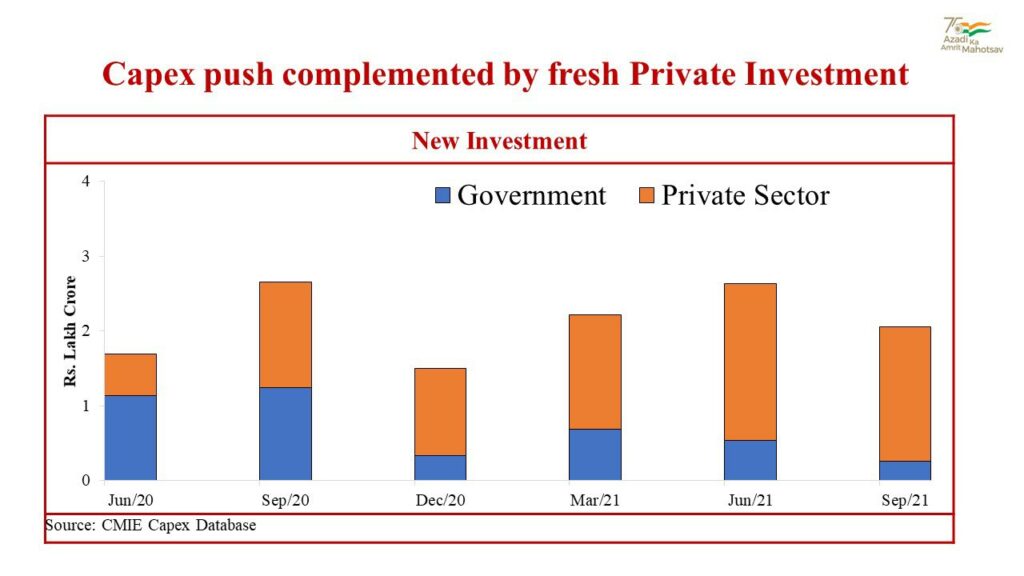

This is partly also due to contribution to investment by the private sector

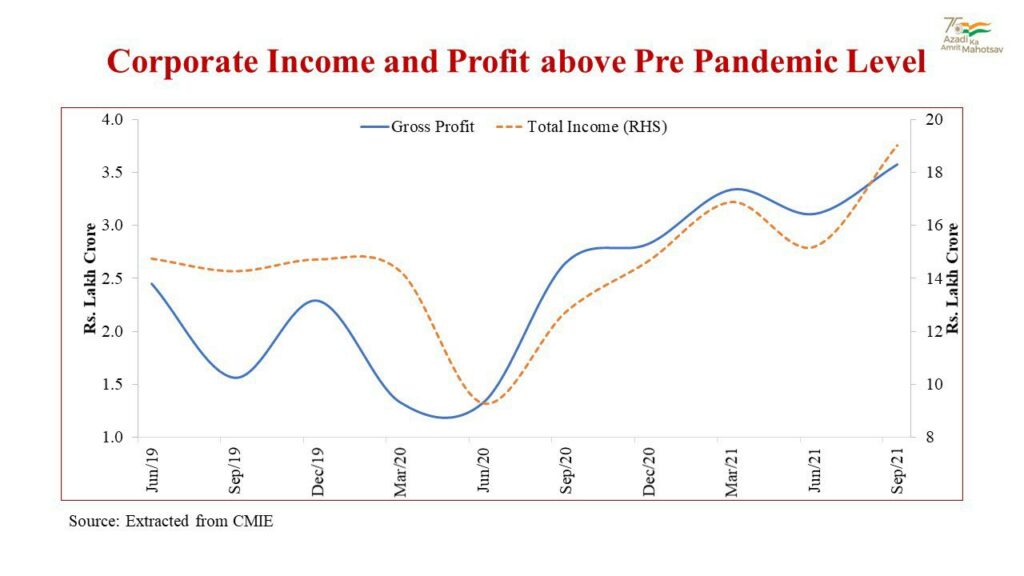

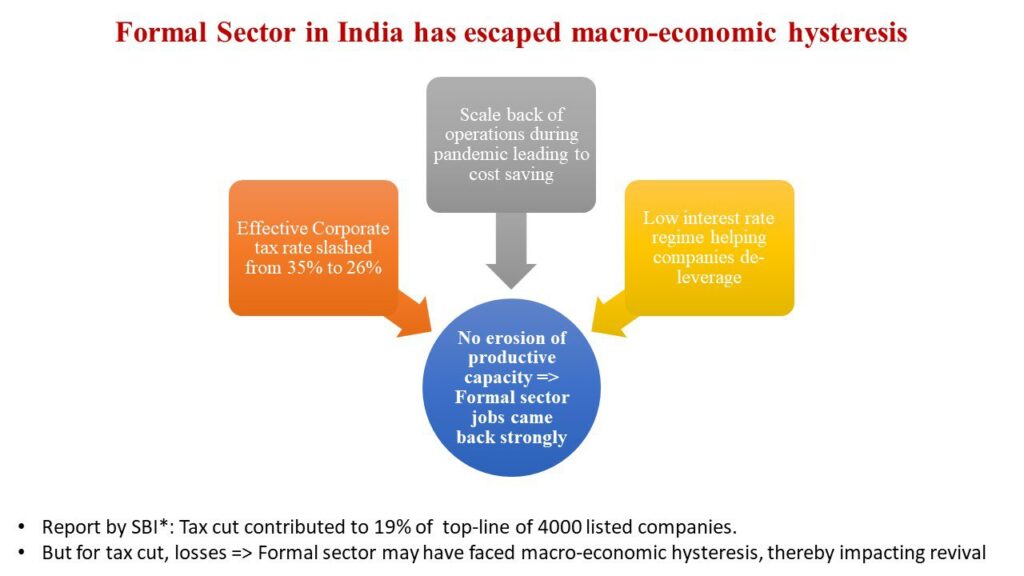

4. Macro-economic hysteresis unlikely because formal sector (more vulnerable because its production relies both on labour & capital) has emerged stronger post-Covid. While informal sector impacted more, hysteresis is unlikely because its production primarily relies on labour.

5. Financial sector has emerged stronger with better asset quality, greater provision coverage as the first line of defence against impending losses from bad loans, and greater capital adequacy as the second line of defence. This is crucial for investment going forward.

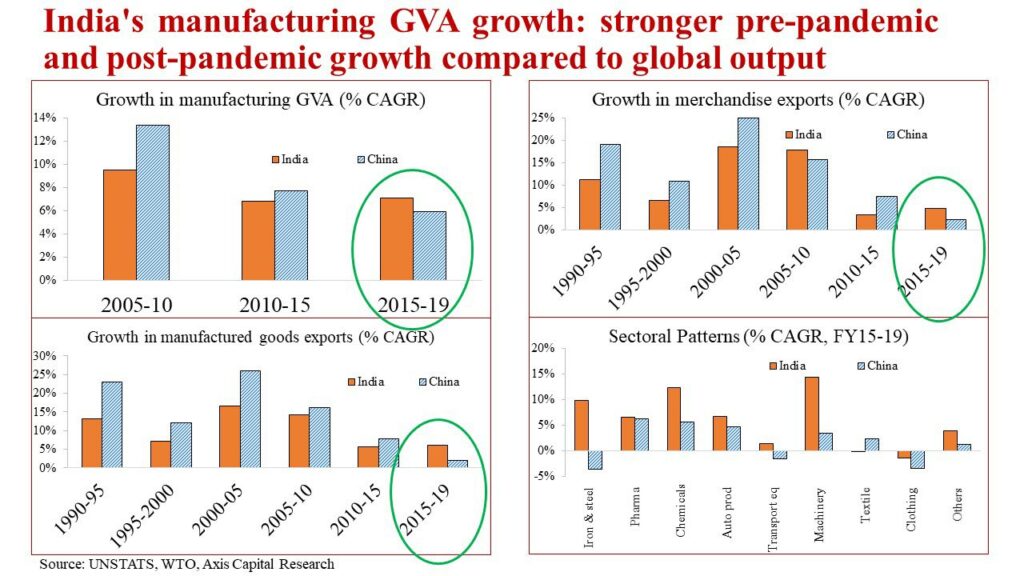

6. Unlike 2005-10 and 2010-15, manufacturing growth in India during 2015-19 has been higher than in China. This has come from the policy focus that has reduced power costs, logistics costs and a competitive tax environment compared to peer economies.