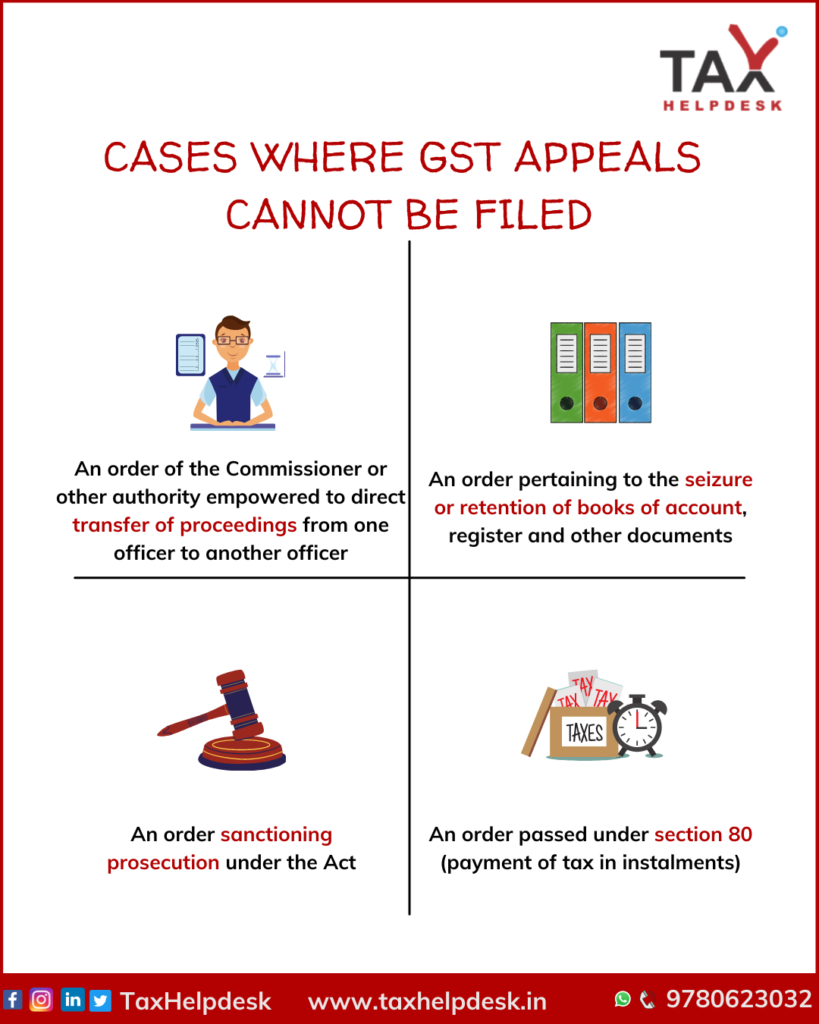

A person who is aggrieved by a decision or order passed against him by an adjudicating authority, can file an appeal to the Appellate Authority and if needed further, to the higher authorities.

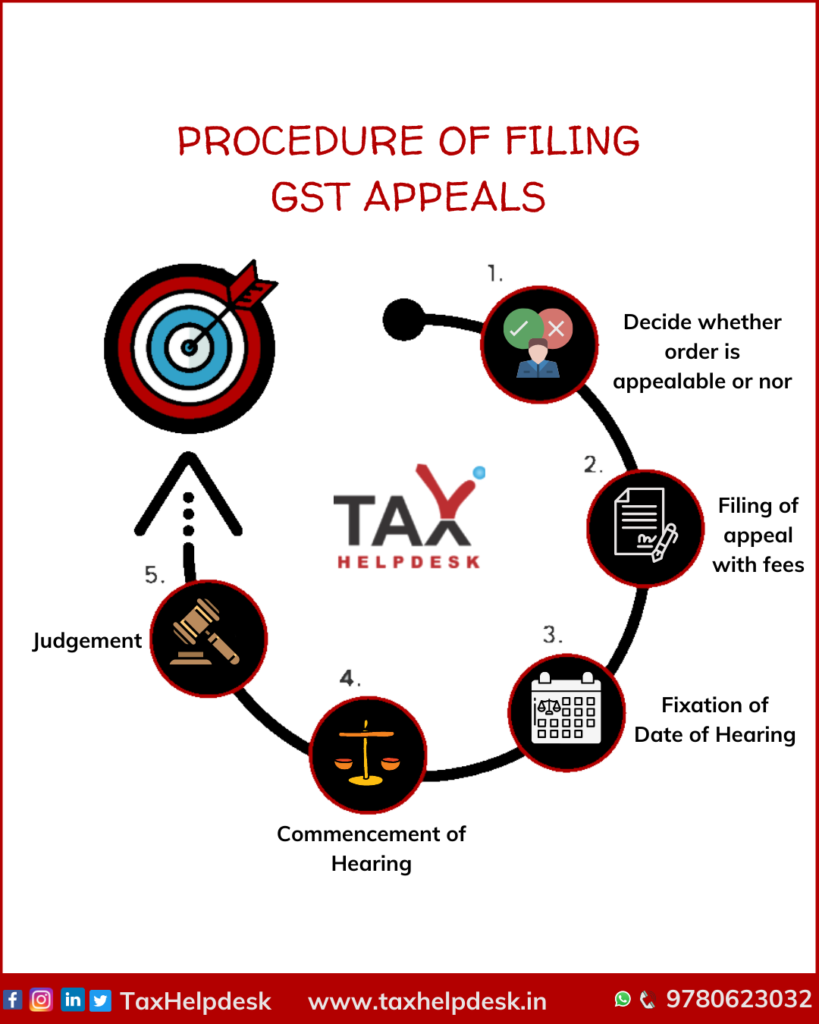

However, appeal is a statutory right and therefore, appeal can not be filed against each order. If you want to know whether the order passed against you is appealable or not or how to get started with filing of appeals, then you are the right platform!

![]()

![]()

Reviews

There are no reviews yet.