- Overview of Goods and Service Tax Registration

- utility of Goods and Service Tax Registration

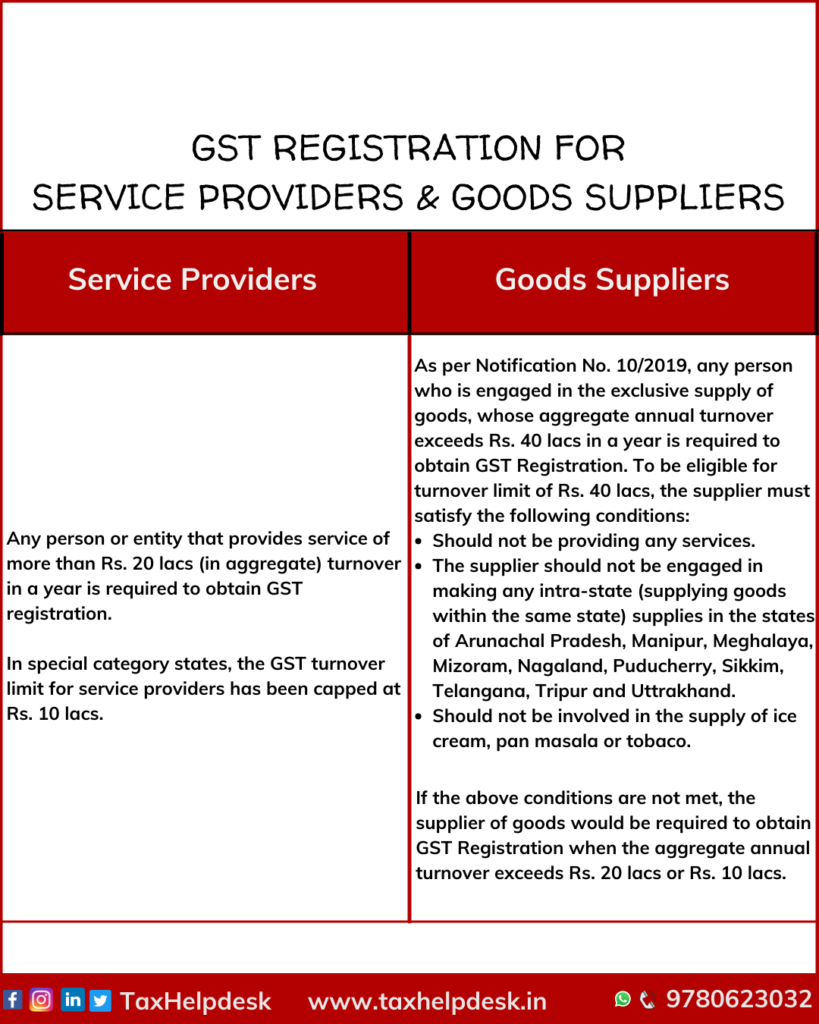

- Who has to obtain GST Registration compulsorily?

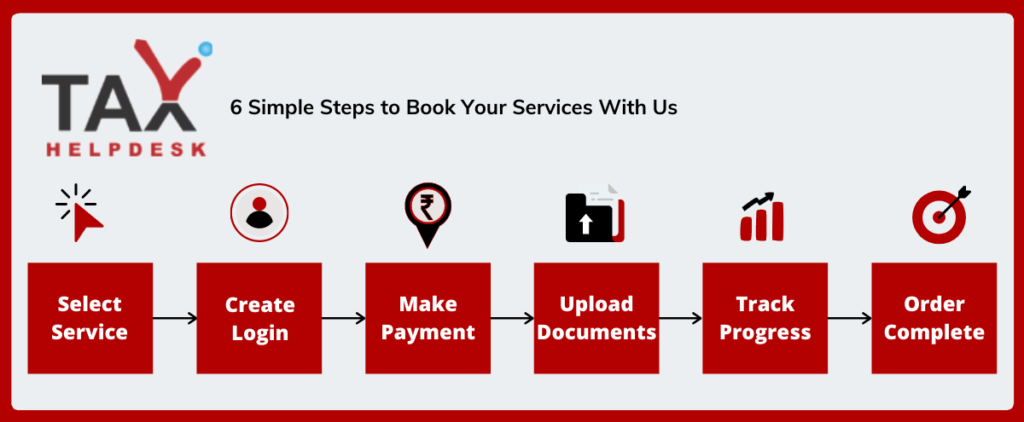

- How to obtain your GST Registration from TaxHelpdesk?

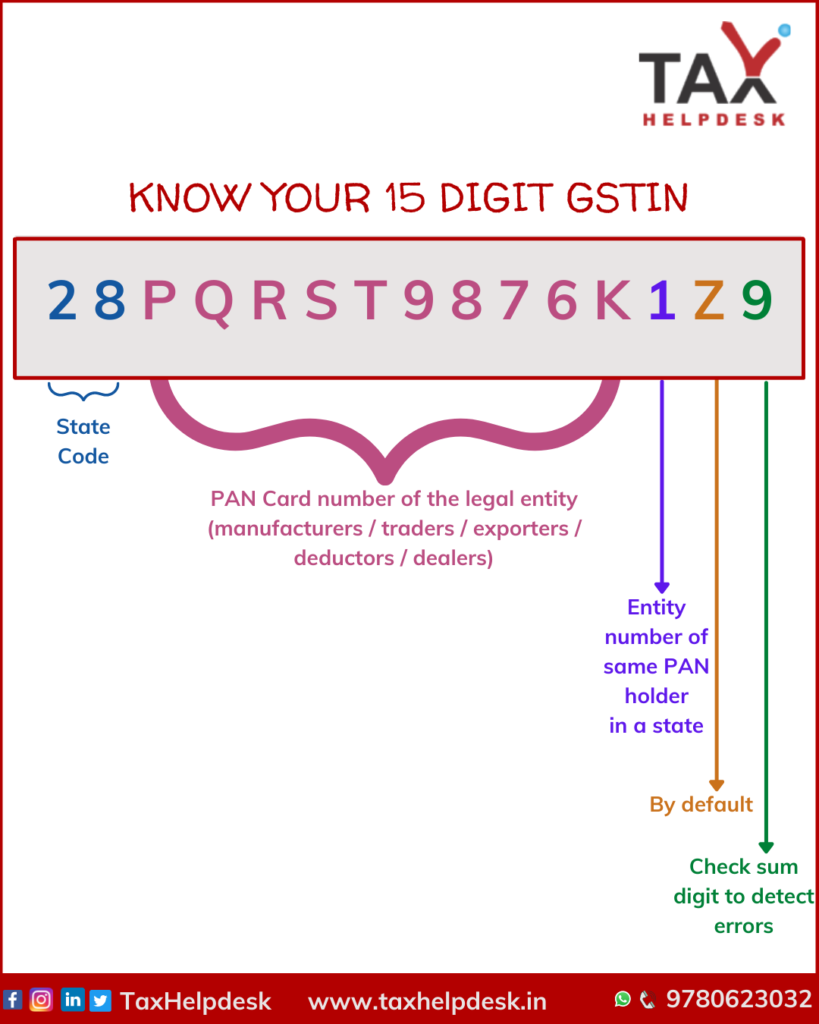

- Structure Of GST Registration/GSTIN

- Types of GST Registration

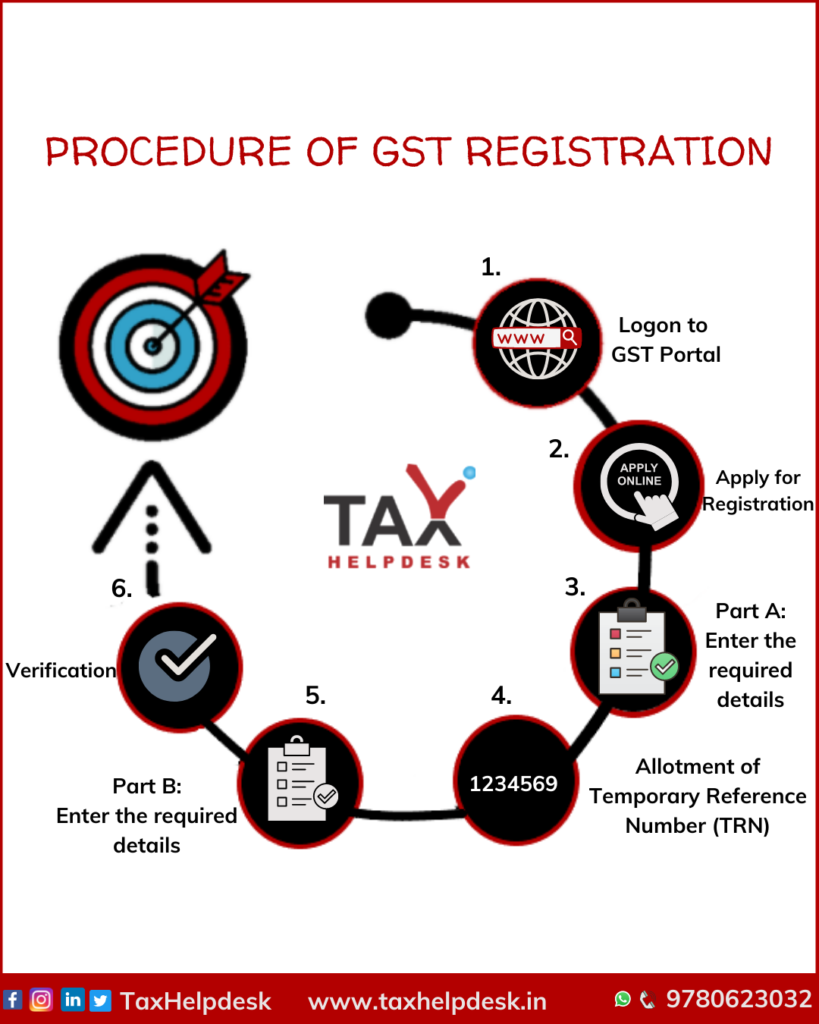

- How to apply for GST Registration?

- Document lists for GST registration

- Time frame for GST Registration

- FAQs

Reviews

There are no reviews yet.