- What is Form GSTR-1?

- Who has to file GSTR-1?

- Get your Income Tax Return filed today by TaxHelpdesk

- Who is exempted from filing?

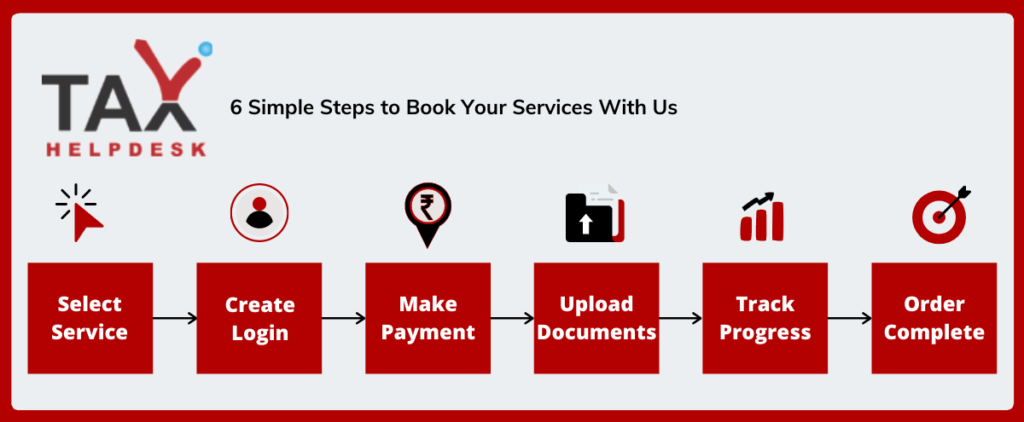

- How to get your GSTR-1 filed by experts at TaxHelpdesk?

- QRMP Scheme

- Contents of GSTR-1 filing

- Due dates for filing

- Late fees for non-filing of GSTR-1

- Procedure of Filing of GSTR-1

- Documents required for GSTR-1 filing

- FAQs

Reviews

There are no reviews yet.