Know Everything About GST ITC on Bank Charges

The ITC on bank charges can be claimed only if it is in furtherance of business. However, there are certain conditions which needs to be fulfilled for availing input tax …

The ITC on bank charges can be claimed only if it is in furtherance of business. However, there are certain conditions which needs to be fulfilled for availing input tax …

Before the advent of the Goods and Services Tax regime, the indirect tax regime comprised of service tax, central excise, VAT and other related taxes. Under the old indirect tax …

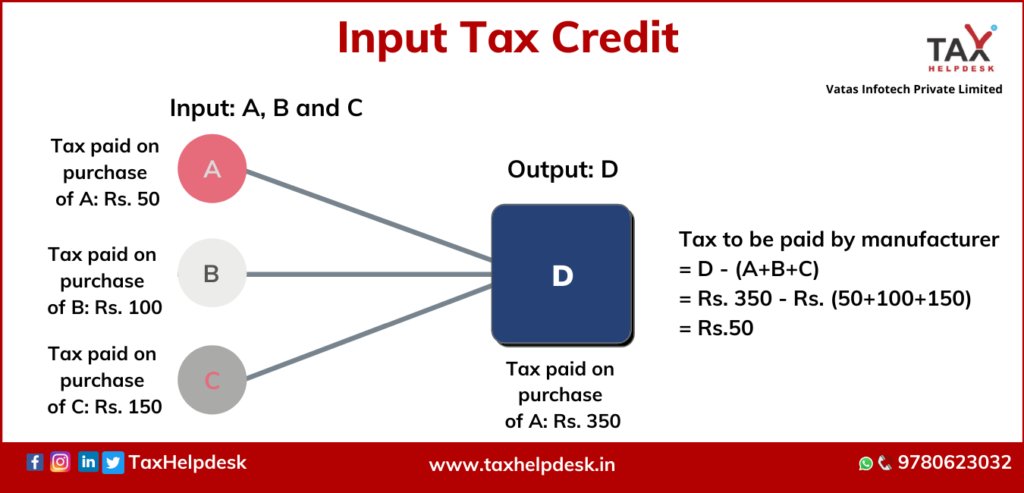

HOW TO CLAIM INPUT TAX CREDIT, ELIGIBILITY & REQUIREMENTS. Read More »

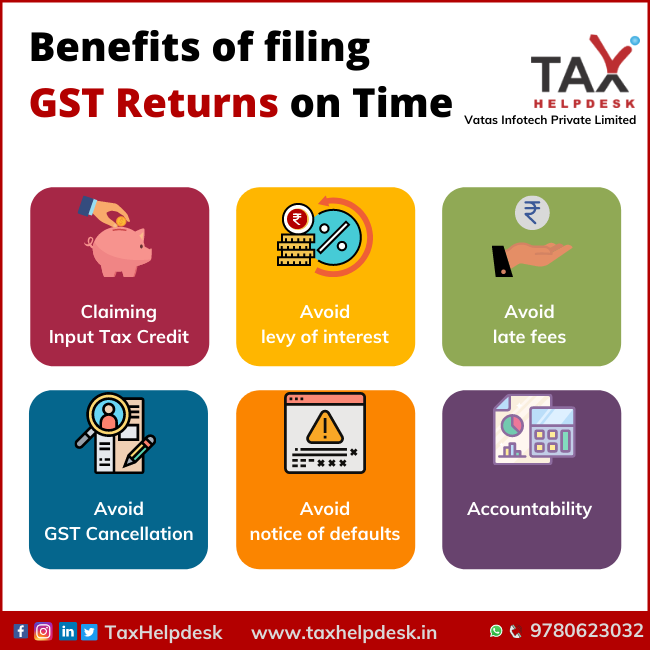

Goods and Services Tax for short: GST Returns is a document that contains all the details of input (purchases), output (sales), input tax (tax paid on purchases) and output tax …

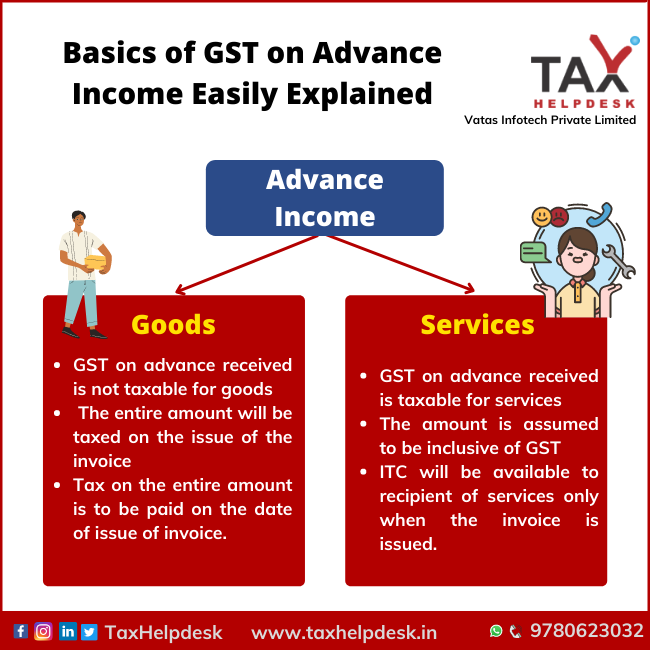

Advance income, as the name suggests is said to be when the payment of income is made before its actual time. This advance income may sometimes be required by the …

Basics of GST on Advance Income Easily Explained Read More »

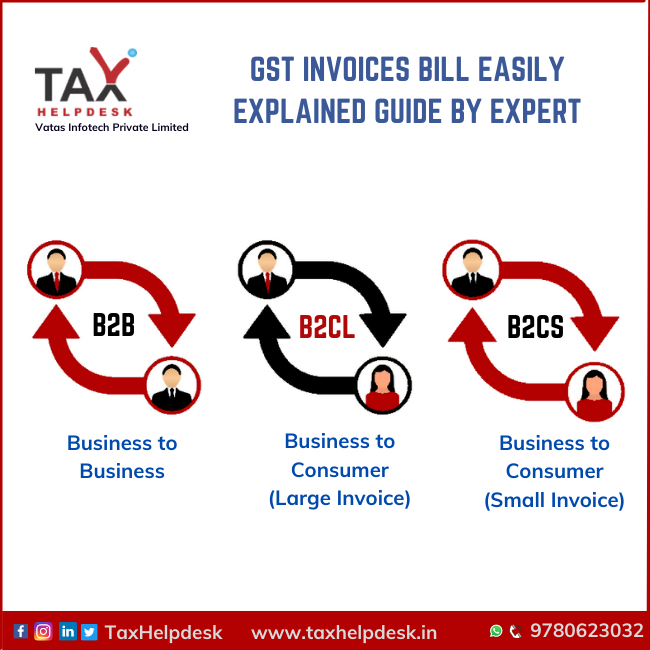

GST Invoices GST invoices are the important documents. This is so because it not only evidences the supply of goods or services but is also an essential document for the recipient …

GST Invoices Bill Easily Explained Guide By Expert Read More »

Compliances play an essential role for taxpayers as well as government. These compliances keeps the checks and balances for each GST registered taxpayer. The GST compliances for month of August, 2021 are as follows:

In order to provide relief to small scale businesses of GST registered taxpayers, the Central Board of Indirect Taxes and Customs has published Quarterly Monthly Payment (QRMP) Scheme. It can be availed by taxpayers having an aggregate turnover of up to Rs. 5 crores.

Time & again various extensions have been provided to taxpayers to comply with filing of returns. GST Compliance for July, 2021 is as follows:

43rd GST Council Meeting heading by Finance Minister Smt. Nirmala Sitharaman was held through video conferencing at New Delhi on May 28, 2021.

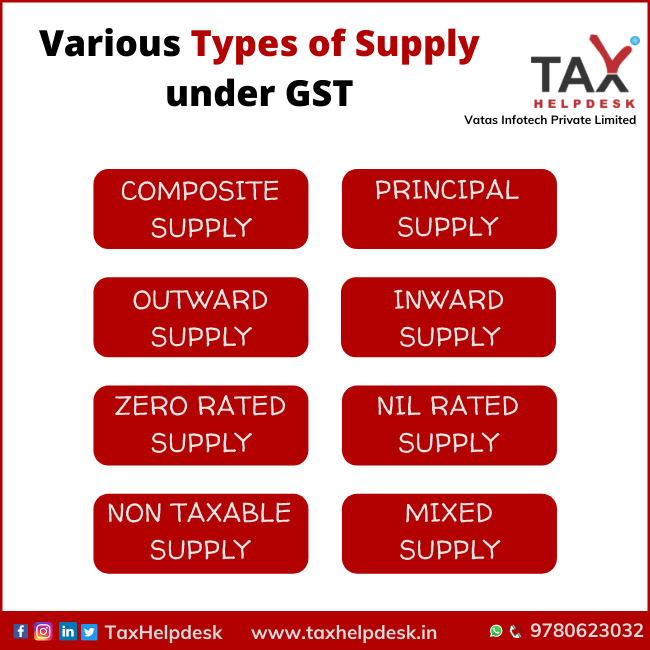

Article 366 of the Indian Constitution defines “goods and services tax” as any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption. The Central and State governments have simultaneous powers to levy GST on Intra-state supply. However, the Parliament alone have exclusive power to make laws with respect to levy of goods and services tax on Inter-state supply.