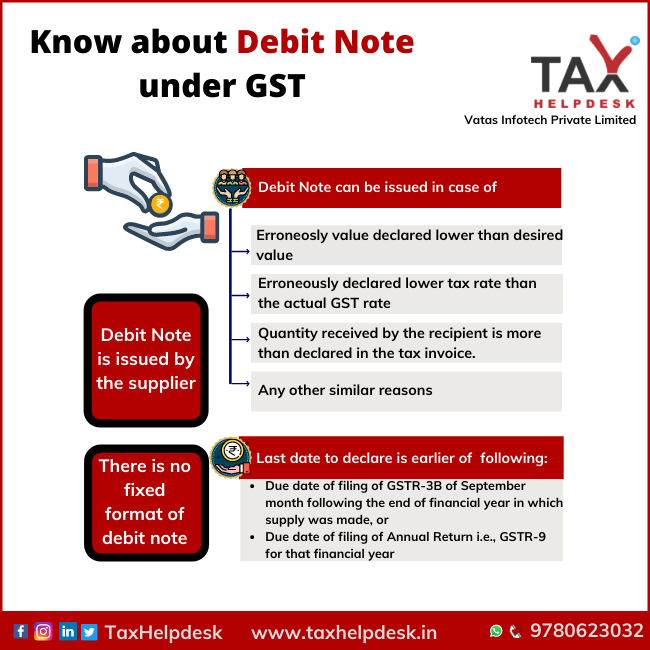

Know About Debit Note Under GST

Debit note under GST is a business/formal document used by the seller to remind the buyer of his current debt obligations, or a document produced by a buyer when returning …

Debit note under GST is a business/formal document used by the seller to remind the buyer of his current debt obligations, or a document produced by a buyer when returning …

Credit Note under GST is issued by the supplier after it has issued the invoice to the buyer. It is applicable under certain circumstances only. Credit Note Credit Note under …

Compliances play an essential role for taxpayers as well as government. These compliances keeps the checks and balances for each GST registered taxpayer. The GST compliances for month of August, 2021 are as follows:

In order to provide relief to small scale businesses of GST registered taxpayers, the Central Board of Indirect Taxes and Customs has published Quarterly Monthly Payment (QRMP) Scheme. It can be availed by taxpayers having an aggregate turnover of up to Rs. 5 crores.

Time & again various extensions have been provided to taxpayers to comply with filing of returns. GST Compliance for July, 2021 is as follows:

nspection, Search or Seizure can only be carried out when an officer, of the rank of Joint Commissioner or above, has reasons to believe the existence of any exceptional circumstances. In such cases the Joint Commissioner may authorise, in writing, any other officer to cause inspection, search and seizure. However, in case of arrests the same can be carried out only where the person is accused of offences specified for this purpose and the tax amount involved is more than specified limit. Further, the arrests under GST Act can be made only under authorisation from the Commissioner.

These compliances details comprises of due dates of Income tax, GST, EPF & PF for June 2021. Having stating this, these Compliances can help the assessee in planning his schedule. …

43rd GST Council Meeting heading by Finance Minister Smt. Nirmala Sitharaman was held through video conferencing at New Delhi on May 28, 2021.

Article 366 of the Indian Constitution defines “goods and services tax” as any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption. The Central and State governments have simultaneous powers to levy GST on Intra-state supply. However, the Parliament alone have exclusive power to make laws with respect to levy of goods and services tax on Inter-state supply.

GST is applicable at the time of supply of goods or services. The origin of goods or services is of no relevance for the purpose of liability to pay tax under GST. Supply is considered to be the main taxable event for charging of tax.